What the Research Actually Shows

Thomas Stanley and William Danko's landmark study "The Millionaire Next Door" (1996, updated findings through subsequent research) surveyed over 1,000 millionaires. The picture that emerged was deliberately anticlimactic: most were first-generation wealth-builders, many were self-employed, most lived in middle-class neighbourhoods, drove practical cars, and accumulated wealth through decades of frugal living and consistent investing — not through extraordinary income or lucky investments.

Ramit Sethi's research and Chris Hogan's "Everyday Millionaires" study (2019, surveying 10,000 US millionaires) reached similar conclusions: 79% received no inheritance. The most common vehicle for building wealth was the workplace 401(k), invested primarily in diversified mutual funds. The typical timeline to millionaire status was 28 years of consistent financial behaviour.

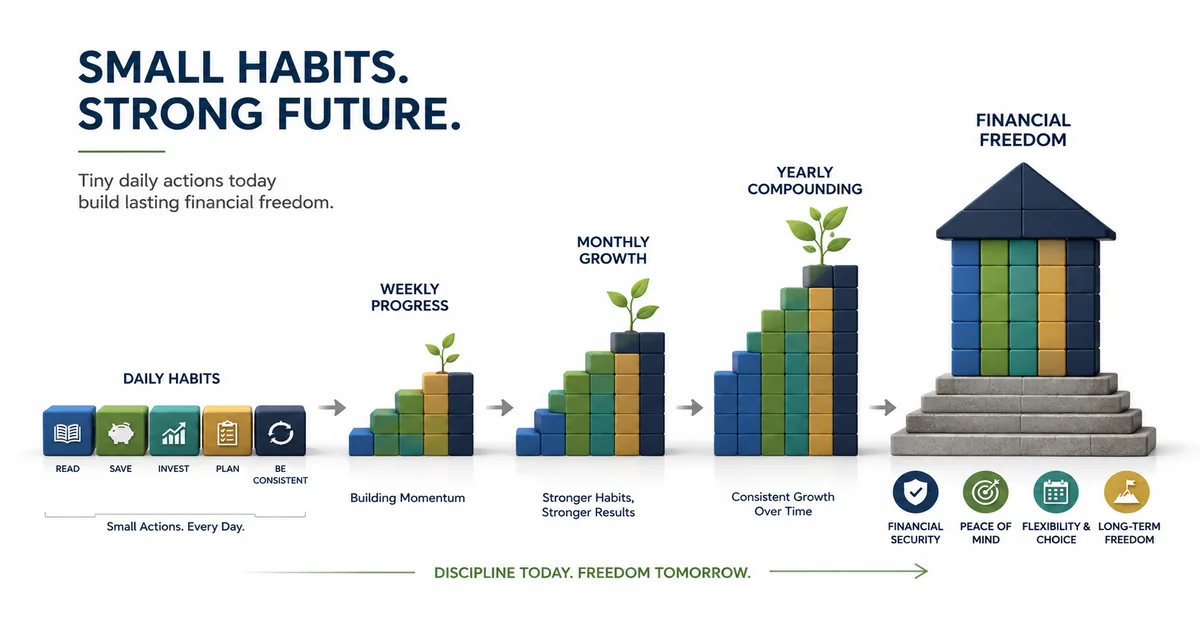

These findings matter because they suggest millionaire status is attainable through replicable habits — not exceptional circumstances.

Habit 1: Live Well Below Your Means

The core paradox of wealth: the people with the highest net worth often display the least of it. First-generation millionaires tend to have high savings rates — not because their incomes are extraordinarily high, but because their spending is deliberately low relative to income.

This doesn't mean deprivation. It means conscious spending — buying what genuinely matters and being indifferent to status symbols that don't. A $70,000 earner who saves 25% of income and invests it over 30 years will typically outperform a $150,000 earner who saves 5%. Savings rate matters more than income level, especially in the early decades.

Avoiding lifestyle inflation — the tendency for spending to rise in lockstep with income — is the practical mechanism. When income increases, the financially successful direct most of the increase to savings rather than consumption.

Habit 2: Invest Consistently, Not Cleverly

The investment strategy of most first-generation millionaires is strikingly simple: regular contributions to diversified, low-cost index funds inside tax-advantaged retirement accounts. Not timing the market. Not individual stock picking. Not alternatives or crypto. The most common holding: total market index funds or S&P 500 index funds, held for decades.

The math behind this is unambiguous. Over any 30-year period in US stock market history, regular investing in a broad index fund has produced significant wealth. The investor's primary job is to keep contributing through volatility and not sell during downturns.

Habit 3: Avoid Consumer Debt Religiously

High-interest consumer debt — credit card balances, personal loans, buy-now-pay-later — is almost universally absent from the financial lives of first-generation wealth-builders. The reason is arithmetic: a 20% credit card rate is a guaranteed 20% negative return on net worth. No investment reliably beats paying off 20% debt.

This doesn't mean avoiding all debt. Mortgages, at historically low rates compared to investment returns, can be wealth-building tools. Student loans for high-ROI education can be justified. The distinction is between debt that finances appreciating assets or rising earning capacity (often worth considering) versus debt that finances consumption (almost always counterproductive).

Habit 4: Invest in Earning Capacity

Saving and investing matters more at higher income levels. Many first-generation millionaires made significant investments in their own skills, education, certifications, and business development — not because they were altruistic about learning, but because higher earnings accelerate wealth-building dramatically.

A $40,000 income with 20% savings produces $8,000 invested per year. A $100,000 income with 20% savings produces $20,000 per year — 2.5× more invested at the same rate. The investment in earning capacity (professional development, advanced education, career moves) is often the highest-return investment available.

Habit 5: Have a Written Financial Plan

Hogan's research found that 97% of millionaires surveyed said they "always" or "often" had a financial plan. The act of writing down specific goals — retirement target, savings rate, debt payoff timeline — significantly increases the probability of achieving them. Plans don't need to be elaborate. A single page with: current net worth, target net worth in 5/10/20 years, monthly savings amount, and investment allocation is sufficient.

The plan gets reviewed annually and updated when circumstances change. It's a commitment device — turning vague intentions into specific, trackable commitments.

Habit 6: Stay Invested Through Volatility

Every major market correction produces articles about "this time being different" and investors who sell at the bottom to avoid further losses. The research is consistent: investors who stay invested through downturns significantly outperform those who move to cash and wait for stability before re-entering.

Selling during a downturn converts a paper loss to a real one and requires getting back in at the right time — which virtually no one does consistently. The simple rule that outperforms most strategies: invest regularly, don't sell during downturns, and stay the course for decades.

Wealth-Building Habits Globally

UK: UK research on wealth-building shows similar patterns — consistent pension contributions, low consumer debt, and modest lifestyles relative to income. The auto-enrolment system builds a foundation, but the truly wealthy in the UK actively supplement with ISA contributions (up to £20,000/year tax-free growth) and property investment. The key UK-specific wealth pattern: property ownership remains the primary wealth vehicle for middle-class wealth accumulation, with pension wealth as the second pillar.

India: India's emerging wealthy middle class shows a strong cultural orientation toward property ownership and gold as wealth stores — both of which have historically preserved value in an inflationary environment. The newer generation of wealth-builders increasingly uses SIPs in equity mutual funds, National Pension System (NPS), and PPF/EPF to build financial asset wealth. A distinctive Indian wealth habit: multi-generational financial support — children supporting parents in retirement is culturally embedded, which affects both the obligation structure and the motivation for wealth-building. SEBI resources at sebi.gov.in.

Canada: Canadian wealth-building mirrors US patterns closely. RRSP (tax-deferred) and TFSA (tax-free) are the primary vehicles. Real estate has been a significant wealth driver in major markets (Vancouver, Toronto). A notable Canadian pattern: the TFSA is underutilised — many Canadians hold cash in their TFSA rather than investing it in equities, missing decades of tax-free compound growth. The habit that separates the wealthier Canadians: maximising TFSA contributions into equity index funds starting early, then supplementing with RRSP for tax deduction benefits. FCAC at canada.ca.