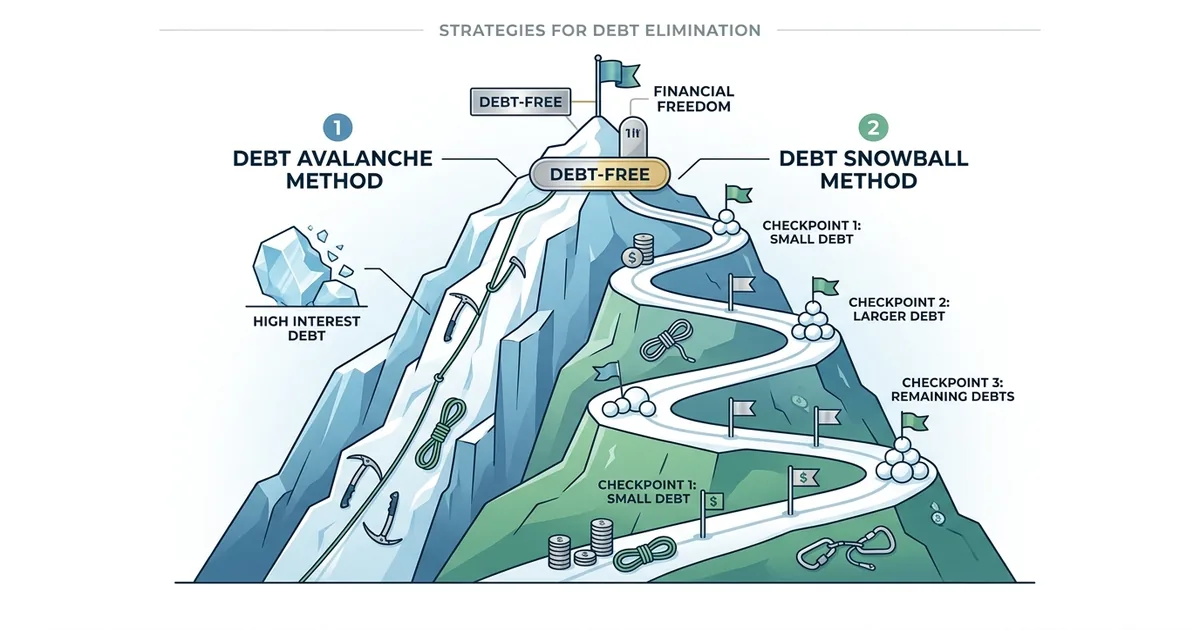

How the Debt Avalanche Works

The avalanche method is mathematically precise. List all your debts, sorted by interest rate from highest to lowest. Pay the minimum on every debt each month. Direct every additional dollar you can toward the debt with the highest interest rate. When that debt is paid off, add its full payment to what you're paying on the next highest-rate debt — the "avalanche" rolling downhill.

Because high-interest debt costs the most per dollar owed, eliminating it first stops the interest bleeding most efficiently. You pay the least total interest possible using this sequence.

How the Debt Snowball Works

The snowball method ignores interest rates entirely and focuses on balance size. List all debts from smallest to largest balance. Pay minimums on all. Direct every extra dollar toward the smallest balance. When it's cleared, roll that payment into the next smallest. The payment amount "snowballs" as each debt is eliminated.

The mechanism is psychological. Paying off a complete account — even a small one — creates a concrete sense of progress that keeps people engaged with the process. Each eliminated account is a visible win. Dave Ramsey popularised this approach specifically because he observed that most debt problems are behaviour problems, not math problems.

Side-by-Side With Real Numbers

Using a realistic debt example: $12,000 in total debt across three accounts, with $300/month of extra money to put toward payoff.

| Debt | Balance | Rate | Min Payment |

|---|---|---|---|

| Credit card A | $4,500 | 24% | $90 |

| Personal loan | $3,200 | 14% | $80 |

| Credit card B | $4,300 | 18% | $86 |

Total minimums: $256/month. Extra: $300/month. Total payment: $556/month.

| Method | Order Attacked | Total Interest Paid | Months to Debt-Free |

|---|---|---|---|

| Avalanche | Card A (24%) → Card B (18%) → Loan (14%) | ~$3,280 | ~28 months |

| Snowball | Loan ($3,200) → Card B ($4,300) → Card A ($4,500) | ~$3,680 | ~28 months |

Illustrative estimates. Actual figures depend on exact payment timing and compound interest. The avalanche saves roughly $400 in this example. Time to debt-free is often similar between methods.

In this example, the avalanche saves about $400 in interest. On larger debt loads with bigger rate differences, the savings can be thousands. But both methods take roughly the same time to clear all debt — because the total extra payments being made are identical.

Which Method Should You Choose?

Choose the avalanche if: you're highly motivated and analytical; you've successfully completed financial goals before; the interest rate difference between your debts is large (e.g., a 28% credit card vs a 6% car loan); or minimising total cost is your primary driver.

Choose the snowball if: you've started and abandoned debt payoff plans before; you have several small debts that feel overwhelming; you know you respond well to short-term wins and visible progress; or you're dealing with the emotional weight of debt and need momentum.

A 2016 Harvard Business Review study found that people who focused on paying off one debt account at a time — regardless of interest rate — were more likely to eliminate all debt than those spreading payments across accounts. The psychological impact of completing a goal, even a small one, was a stronger motivator than the rational financial calculation.

The Hybrid Approach

You don't have to choose rigidly. A hybrid strategy takes the best of both: start by wiping out one very small debt quickly (snowball) to build confidence and momentum, then switch to avalanche order for the remaining debts. This works well when you have one or two very small debts (under $500) that could be cleared in a month or two, followed by larger high-interest balances where the avalanche's math really pays off.

Debt Management Globally

UK: The same avalanche and snowball principles apply to UK consumer debts. The average UK household carries credit card debt, personal loans, and student loans (which work differently — income-contingent repayment). StepChange, the UK's largest debt charity, offers free debt advice and structured repayment plans at stepchange.org. MoneyHelper has comprehensive debt guidance at moneyhelper.org.uk.

India: Consumer debt in India includes credit card debt (with very high APRs of 36–42%), personal loans, EMI purchases, and vehicle loans. The avalanche method is particularly powerful in India given the very high interest rates on revolving credit card debt. The RBI mandates transparency on interest rates and charges at rbi.org.in. Prepayment on most personal loans is allowed (though some lenders charge a prepayment fee).

Canada: Canadian consumer debt patterns are similar to the US. The FCAC (Financial Consumer Agency of Canada) offers a debt repayment calculator and budgeting tools at canada.ca. Non-profit credit counselling agencies across provinces provide free debt management help for Canadians overwhelmed by multiple debts.

"Personal finance is more personal than finance. The best debt payoff method isn't the one that saves the most on paper — it's the one that keeps you going when motivation dips. I've seen clients paid off with the snowball who would have given up halfway through an avalanche plan."