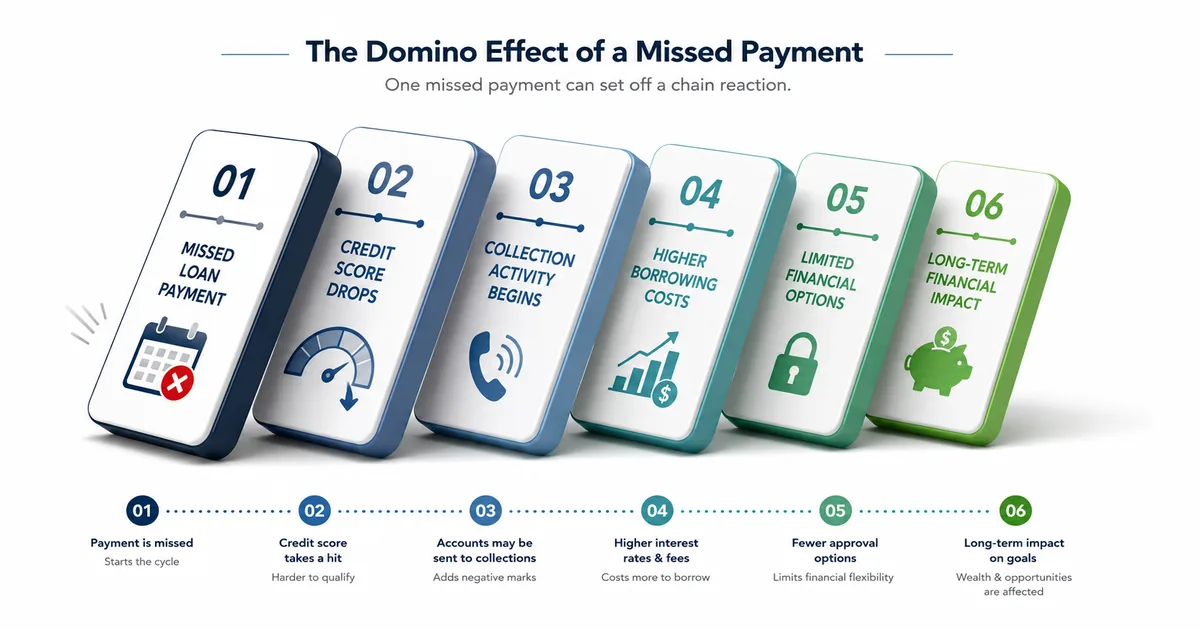

The Automatic Stay — Immediate Protection

The moment you file for bankruptcy, the automatic stay immediately stops most collection activity: collection calls, letters, lawsuits, wage garnishment, bank levies, and foreclosure proceedings. This breathing room is often the most immediate benefit of filing — it gives you time to address your financial situation without the pressure of ongoing collection.

The stay is temporary. For Chapter 7, it ends when the bankruptcy is discharged or dismissed. For Chapter 13, it remains in effect throughout the repayment plan. Creditors can petition the court to lift the stay for secured creditors (like a mortgage lender) under certain circumstances. Source: uscourts.gov.

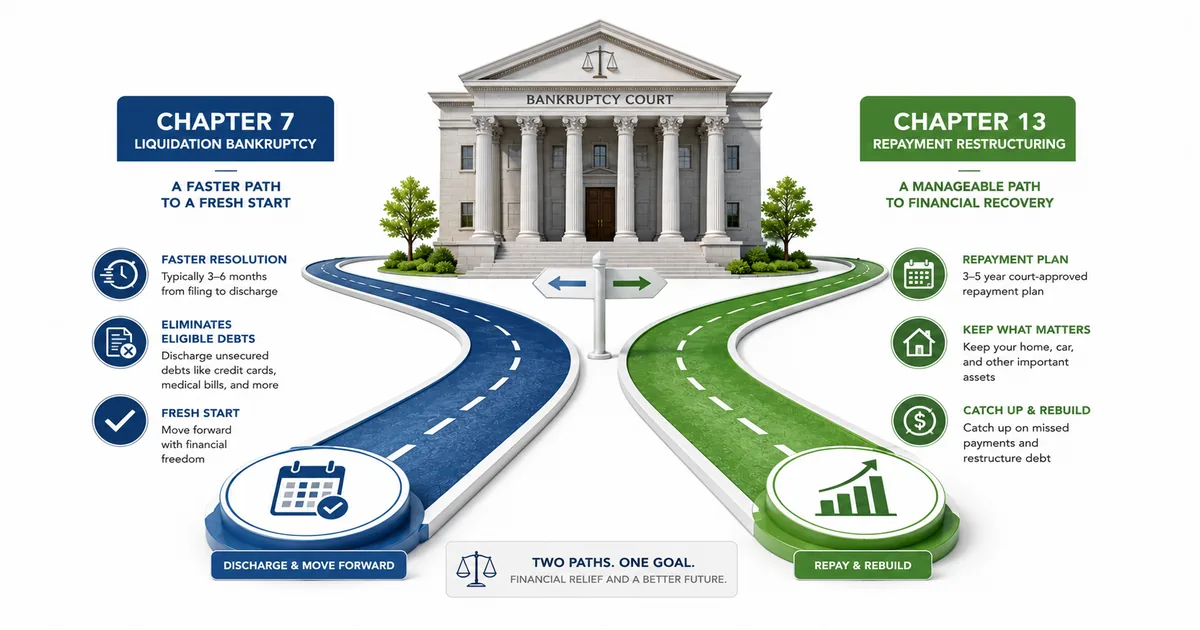

Chapter 7: Liquidation Bankruptcy

Chapter 7 is the faster and simpler form. A court-appointed trustee reviews your assets, sells non-exempt property to pay creditors, and discharges most remaining unsecured debt. The entire process typically takes 3–6 months.

Means test: To qualify, your household income must be below the state median income for your household size — or you must pass a more detailed calculation showing you don't have enough disposable income to repay debts. The test exists to prevent higher-income filers from using Chapter 7 to discharge debt they could repay.

Exempt assets: Federal and state law exempt certain assets from liquidation — you keep them. Common exemptions: a portion of home equity (homestead exemption, varies by state), personal vehicle up to a value, retirement accounts (401k, IRA fully protected under federal law), essential household goods, and tools of your trade. Exemption amounts vary significantly by state.

What's discharged: Credit card debt, medical bills, personal loans, utility arrears, and most other unsecured consumer debt. Not dischargeable: Student loans (in most cases), recent tax debts, child support, alimony, and debts from fraud or criminal activity.

Chapter 13: Reorganisation Bankruptcy

Chapter 13 is the "repayment plan" bankruptcy. You propose a 3–5 year repayment plan to the court, making monthly payments to a trustee who distributes funds to creditors. At the end of the plan, remaining eligible unsecured debt is discharged.

Key advantages over Chapter 7: You keep all assets (no liquidation). You can save your home from foreclosure by catching up on arrears through the plan. Non-dischargeable debt in Chapter 7 (some tax debts, domestic support arrears) can be addressed in Chapter 13's repayment structure. You can strip a second mortgage from a home worth less than the first mortgage balance.

Requirements: Regular income to fund the plan. Unsecured debt below $2,750,000 and secured debt below $1,395,875 (2026 limits). Complete the repayment plan successfully — if income drops and you can't fund the plan, the case may be dismissed or converted to Chapter 7.

Side-by-Side Comparison

| Feature | Chapter 7 | Chapter 13 |

|---|---|---|

| Timeline | 3–6 months | 3–5 years |

| Asset protection | Exempt assets only; others liquidated | Keep all assets |

| Income requirement | Must pass means test | Must have regular income |

| Home foreclosure | Cannot stop foreclosure long-term | Can cure arrears through plan |

| Credit report | 10 years | 7 years |

| Best for | Few assets, primarily unsecured debt, lower income | Keep home, higher income, non-exempt assets |

Long-Term Consequences

Credit: Chapter 7 stays on your credit report for 10 years; Chapter 13 for 7 years. Initial score drop of 150–200 points is typical. Recovery is possible — with responsible credit use post-bankruptcy, scores can recover to 650–700 within 2–3 years.

Future borrowing: Getting credit, a mortgage, or renting an apartment is harder for years after filing. FHA mortgage loans are available 2 years after Chapter 7 discharge; conventional loans typically 4 years.

Employment: Some employers check credit history — government, financial services, and security-clearance positions may be affected.

Alternatives to Consider First

Before filing, exhaust these alternatives: negotiate directly with creditors (many prefer payment arrangements to bankruptcy losses); work with a nonprofit credit counselling agency on a Debt Management Plan; explore debt consolidation loans; consult with a bankruptcy attorney about whether alternatives make financial sense given your specific situation.

Bankruptcy Globally

UK: UK individual insolvency options include Bankruptcy (similar to Chapter 7 — typically 12 months before discharge, assets sold), Individual Voluntary Arrangement (IVA — like Chapter 13, 5-6 year repayment plan, formal legal protection from creditors), and Debt Relief Orders (DRO — for lower income/assets, 12-month moratorium then discharge). Bankruptcy in the UK stays on record for 6 years. Insolvency Service at gov.uk.

India: India's Insolvency and Bankruptcy Code (IBC) 2016 includes provisions for individual insolvency (Part III), though the individual insolvency framework is still being implemented for personal insolvency beyond guarantors. The process is handled through the Debt Recovery Tribunal (DRT) and NCLT. In practice, most Indian consumer debt distress is handled through bank restructuring, one-time settlement (OTS), or simply asset recovery.

Canada: Canadian personal insolvency options include Bankruptcy (similar to Chapter 7 — automatic discharge in 9 months for first-time filers with no surplus income) and Consumer Proposal (similar to Chapter 13 — up to 5 years, pay fraction of debt, administered by Licensed Insolvency Trustee). Consumer proposals are increasingly popular because they cause less credit damage and creditors often prefer them. Both appear on credit report for 6–7 years. OSB at canada.ca.