Delinquency vs Default

These terms are often confused but describe different stages of payment failure:

Delinquency begins the day after a payment is due and not made. You're 30-day delinquent, 60-day delinquent, or 90-day delinquent based on how many days have passed since the due date. Lenders typically report to credit bureaus after 30 days of non-payment — earlier reporting is less common but possible.

Default is a more formal status that varies by loan type:

- Credit cards: typically at 180 days (6 months) of non-payment

- Personal loans: typically at 90–120 days

- Mortgages: typically at 90–120 days, then foreclosure process begins

- Federal student loans: at 270 days (9 months) of non-payment

- Private student loans: typically at 90–120 days

Default represents a formal declaration by the lender that the loan agreement has been breached. At this point, the lender may demand the entire remaining balance immediately (acceleration clause) and begin more serious collection activity.

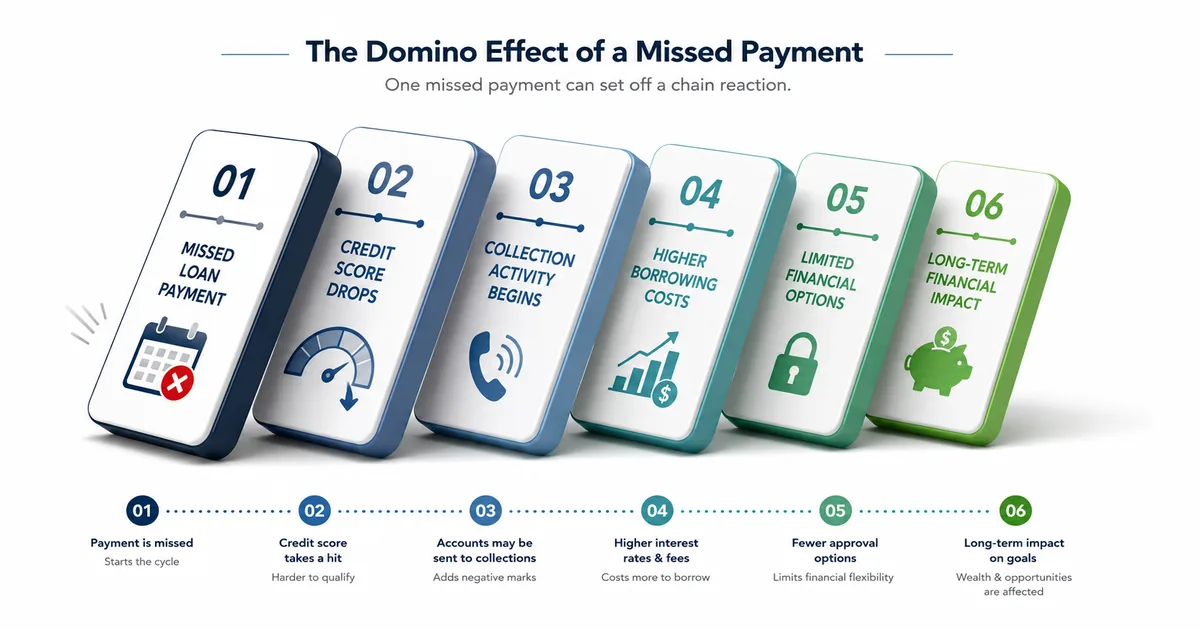

The Default Cascade — What Happens Step by Step

Days 1–29 (missed payment): You're delinquent but the lender may not report yet. You'll receive calls and written notices. Late fees apply — typically $25–$40. This is the easiest point to resolve by making the payment.

Days 30–89 (30–60 day delinquency): The late payment is reported to credit bureaus. Your credit score drops — potentially 50–100+ points. The lender's collection department contacts you more aggressively. Many lenders have hardship programs — call and ask before this stage.

Days 90–180 (pre-default): More serious. The lender may start formal collection procedures. For credit cards, this is when charge-off begins to approach.

Charge-off: The lender writes your debt off its books as a loss. This does NOT eliminate your obligation to pay — it just means the lender has given up trying to collect internally and will transfer the debt. A charge-off shows on your credit report as a separate negative item and is very damaging.

Debt sale to collection agency: The lender sells your debt (typically for 5–15 cents on the dollar) to a third-party debt collector. The collector now owns the debt and will pursue collection. You may receive less friendly communication from this point. A new collection account appears on your credit report.

Legal action: The collector (or original lender) may sue you for the amount owed. If they win, they receive a court judgment — a legal right to collect via wage garnishment, bank levy, or property liens.

Wage garnishment: With a court judgment, a creditor can garnish up to 25% of your disposable income (after mandatory deductions) per federal law. Some states have lower limits or exempt certain income types.

Credit Score Impact

A single missed payment reported to credit bureaus can cause significant damage, especially from a high starting score:

- From a 780 score: a 30-day late payment can drop 90–110 points

- From a 680 score: the same late payment drops 60–80 points

- A charge-off or collection: an additional 50–100 points

These items remain on your credit report for 7 years from the date of the original delinquency. Their score impact diminishes over time as new positive activity accumulates — but a default at 30 will still affect you at 37. Paying a collection account doesn't remove it from your report (though it changes the status to "paid"), but can improve your score depending on which scoring model a lender uses.

What to Do If You're Struggling to Pay

The most important principle: act early. Your options shrink dramatically once you've defaulted.

Before missing a payment: Call your lender and explain your situation. Most lenders have hardship programs — temporary payment reduction, interest rate reduction, or payment deferral. These are rarely advertised but widely available. The lender would rather you pay something than nothing.

After missing 1–2 payments: Still call. Arrangements are possible at this stage. Ask specifically about hardship programs, forbearance, or loan modification.

In full default — collection stage: Understand your rights (below). Consider working with a nonprofit credit counsellor (NFCC.org). Evaluate debt management plans. For very large debt burdens, consult a bankruptcy attorney — a Chapter 7 or Chapter 13 filing may stop collection immediately through the automatic stay.

Your Rights with Debt Collectors

The Fair Debt Collection Practices Act (FDCPA) protects you from abusive collection practices. Key rights:

- Collectors cannot call before 8 AM or after 9 PM

- You can request in writing that they stop contacting you — they must then stop except to notify you of specific actions (lawsuit, etc.)

- They cannot threaten actions they don't intend to take or don't have the legal right to take

- You have 30 days from first contact to request written verification of the debt

- They cannot discuss your debt with third parties (except your attorney)

Report FDCPA violations to the CFPB at consumerfinance.gov and the FTC. Also verify that any debt being collected is legitimate and within the statute of limitations for your state — time-barred debt cannot be used to sue you, though collectors may still attempt to collect.

Loan Default Consequences in the UK, India, and Canada

UK: After missing payments, UK lenders issue default notices. A formal default is registered with credit reference agencies (Experian, Equifax, TransUnion UK) and remains for 6 years — not 7 as in the US. Creditors can apply to the court for a County Court Judgment (CCJ), which is the UK equivalent of a US court judgment and enables enforcement. Wages can be garnished through an Attachment of Earnings Order. The FCA regulates debt collection practices — collectors must treat debtors fairly under the FCA's Consumer Duty rules. StepChange at stepchange.org provides free debt advice.

India: Lenders in India report defaults to credit bureaus (CIBIL, Equifax, Experian, CRIF). A poor CIBIL score makes future borrowing very difficult. For secured loans (home, car), the SARFAESI Act allows banks to take possession of pledged assets without court intervention after issuing notices. For unsecured debts, recovery is through civil courts (Debt Recovery Tribunals for larger amounts). Debt collection practices are regulated by the RBI's Fair Practices Code — collectors cannot harass borrowers outside specified hours. RBI guidelines at rbi.org.in.

Canada: Missed payments are reported to Equifax Canada and TransUnion Canada. Provincial limitations periods (2–6 years depending on province) limit how long creditors can sue — after that, the debt is legally unenforceable even if it appears on credit reports. Wage garnishment requires a court judgment (except for CRA tax debts). Consumer proposals and bankruptcy are handled by Licensed Insolvency Trustees and provide protection from creditors through an automatic stay. FCAC at canada.ca.