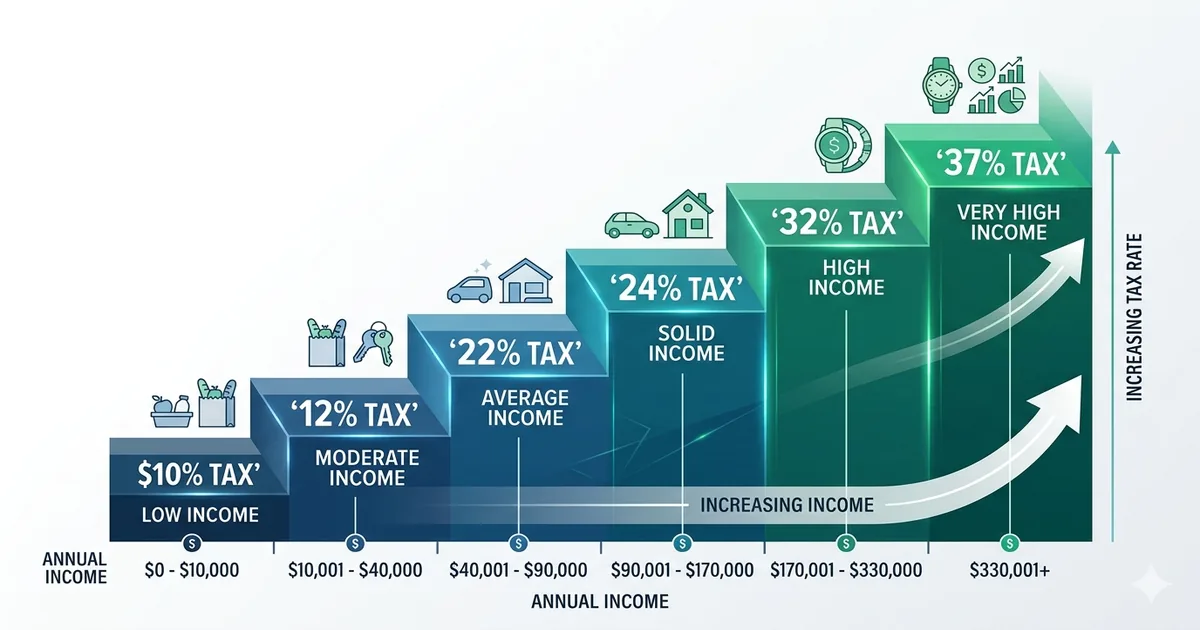

How Tax Brackets Actually Work

Think of your income as filling a series of buckets. The first bucket holds up to $11,925 of taxable income and is taxed at 10%. Once that bucket is full, the overflow goes into the next bucket (12%), and so on. Only income that overflows into the highest bracket gets taxed at that rate.

This is why a raise never costs you money. If you earn $47,000 and get a $5,000 raise, the extra $5,000 falls in the 22% bracket — but only that $5,000 is taxed at 22%. Your original $47,000 is still taxed at the same rates as before. You always take home more from a raise.

2026 Federal Tax Brackets

| Tax Rate | Single Filer Taxable Income | Married Filing Jointly |

|---|---|---|

| 10% | Up to $11,925 | Up to $23,850 |

| 12% | $11,925 – $48,475 | $23,850 – $96,950 |

| 22% | $48,475 – $103,350 | $96,950 – $206,700 |

| 24% | $103,350 – $197,300 | $206,700 – $394,600 |

| 32% | $197,300 – $250,525 | $394,600 – $501,050 |

| 35% | $250,525 – $626,350 | $501,050 – $751,600 |

| 37% | Above $626,350 | Above $751,600 |

Source: IRS Rev. Proc. 2025-40. These are taxable income brackets — income after subtracting the standard deduction ($15,000 single / $30,000 MFJ in 2026). Always verify current figures at irs.gov.

Marginal Rate vs Effective Rate

These two numbers confuse many people:

Marginal rate = the tax rate that applies to your next dollar of income. If you earn $80,000 as a single filer, your marginal rate is 22% — because the next dollar you earn falls in the 22% bracket.

Effective rate = your total federal income tax divided by your total taxable income. This is what you actually pay, on average, across all your income. For a $80,000 earner, the effective rate is roughly 13% — much lower than the 22% marginal rate, because the first portions of income were taxed at 10% and 12%.

The effective rate is the more meaningful number for understanding your actual tax burden. The marginal rate matters when evaluating decisions at the margin — like whether additional income from a side job is worth it, or how much a deduction actually saves you.

A Worked Example

Let's calculate the actual federal income tax for a single filer with $80,000 of gross income in 2026:

- Subtract the standard deduction: $80,000 − $15,000 = $65,000 taxable income

- Apply brackets:

- 10% on first $11,925 = $1,193

- 12% on $11,925–$48,475 ($36,550) = $4,386

- 22% on $48,475–$65,000 ($16,525) = $3,636

- Total federal income tax = $1,193 + $4,386 + $3,636 = $9,215

- Effective rate = $9,215 ÷ $65,000 = 14.2%

This person is in the 22% bracket but pays an effective federal income tax rate of about 14%. Add FICA taxes (Social Security 6.2% + Medicare 1.45% = 7.65% on wages) and their total federal tax burden is approximately $15,337, or about 19% of gross income.

How to Reduce Your Taxable Income

The standard deduction ($15,000 single, $30,000 married filing jointly in 2026) reduces taxable income automatically. Beyond that:

- 401(k) / 403(b) contributions reduce taxable income dollar-for-dollar. A $23,500 401(k) contribution in 2026 saves someone in the 22% bracket $5,170 in federal income tax.

- Traditional IRA contributions (if deductible) — up to $7,000 ($8,000 if 50+).

- HSA contributions — up to $4,300 individual / $8,550 family in 2026.

- Student loan interest — up to $2,500 deductible (subject to income limits).

- Self-employment deductions — half of self-employment tax, business expenses, SEP-IRA contributions.

Income Tax Systems in the UK, India, and Canada

UK — Income Tax Bands: The UK also uses a progressive tax system. The Personal Allowance (tax-free income) is £12,570 for 2026/27. Income above this is taxed at: 20% Basic Rate (£12,571–£50,270), 40% Higher Rate (£50,271–£125,140), and 45% Additional Rate (above £125,140). National Insurance contributions (similar to US Social Security/Medicare) add an additional 8% on earnings between £12,570–£50,270. The effective rate is always below the marginal rate for the same reasons as the US. Current rates at gov.uk/income-tax.

India — Income Tax Slabs: India has two tax regimes from which taxpayers can choose annually. The new regime (default from FY 2024-25) has slabs of: 0% up to ₹3 lakh, 5% on ₹3–7 lakh, 10% on ₹7–10 lakh, 15% on ₹10–12 lakh, 20% on ₹12–15 lakh, and 30% above ₹15 lakh. The old regime has different slabs but allows deductions (80C, 80D, HRA, etc.) that can significantly reduce taxable income. A rebate under Section 87A makes income up to ₹7 lakh effectively tax-free under the new regime. Details at incometaxindia.gov.in.

Canada — Federal Tax Brackets: Canada's federal tax rates for 2026 are: 15% on the first $57,375, 20.5% on $57,375–$114,750, 26% on $114,750–$158,519, 29% on $158,519–$220,000, and 33% on income above $220,000. Provincial income taxes are added on top — total effective rates vary by province. The Basic Personal Amount of ~$16,129 is non-refundable tax credit that effectively makes that income tax-free. More at canada.ca.